The bears are pricing seat compression. They're missing the consumption layer being built on top.

The SaaS apocalypse is a tidy story. AI eats workflows. Seats compress. Systems of record become legacy. Sell the incumbents. The numbers tell a different story. So does the architecture.

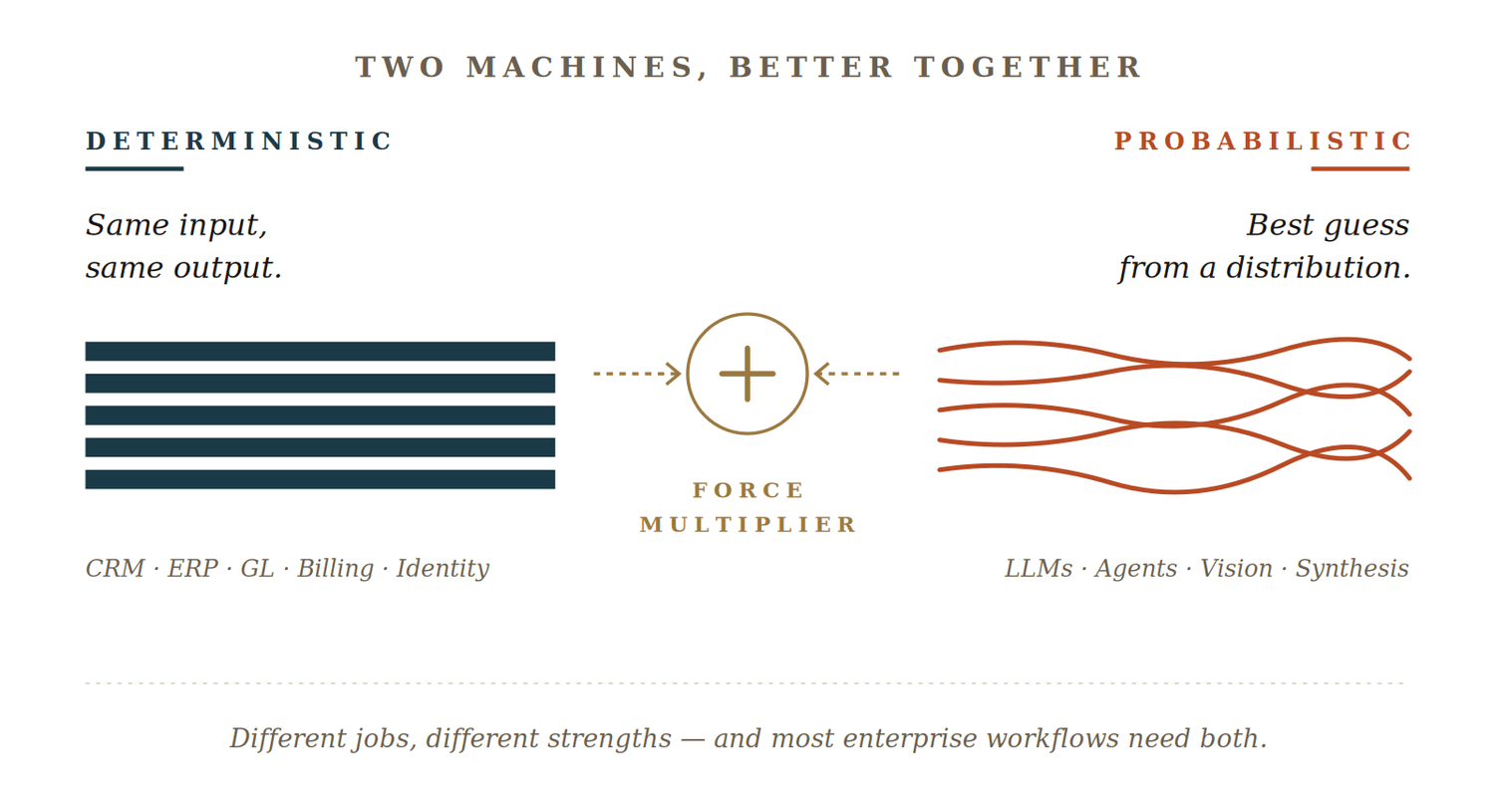

I. Two Machines, Different Jobs

Software now comes in two flavors. Deterministic systems — CRM, ERP, GL, billing, identity — do the same thing every time. Auditable, reproducible, non-negotiable in high-stakes workflows. Probabilistic systems — LLMs, agents, vision models — bring versatile judgment but are non-reproducible by design.

They aren't competitors. They complement. Where stakes are high, deterministic still wins. Where work is open-ended, probabilistic shines. In the enormous middle, they work best together — AI orchestrating across deterministic systems of record, multiplying their value rather than replacing them.

II. The Mispricing

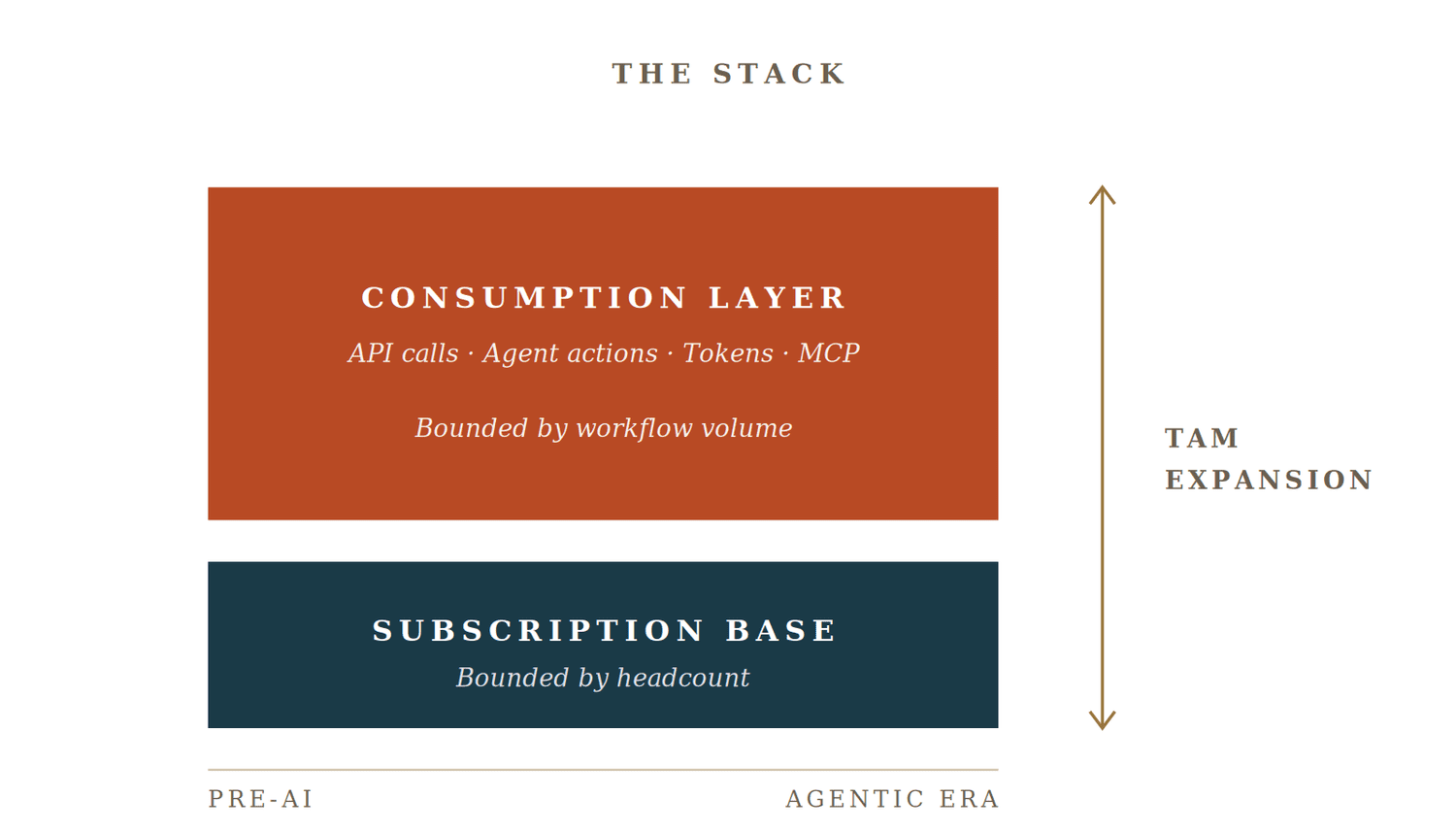

Here's what most takes miss: the agentic layer isn't just a defensive hedge for SaaS incumbents. It is structural TAM expansion.

Per-seat pricing is bounded by headcount. A 10,000-person customer has a ceiling. Consumption-based monetization — API calls, agent actions, tokens, MCP invocations — is bounded by workflow volume. Agents don't sleep, take lunch, or context-switch. They transact orders of magnitude more than humans ever did.

Every workflow that lived behind a UI as a "free" feature becomes a billable, metered unit when an agent calls it. The product surface didn't grow. The monetizable surface did.

III. The Receipts

This isn't theoretical. It's already in the revenue line.

- Salesforce — Agentforce ARR, Q4 FY26. Combined Agentforce + Data 360 ARR is now $2.9B, up 200%+. FY30 target raised to $63B. $800M · +169%

- ServiceNow — 2026 AI ACV target raised 50% above prior guidance. $1M+ Now Assist customers grew 130%+ Y/Y. ~$1.5B

- Microsoft — Commercial RPO, Q2 FY26 — contracted future revenue. M365 Copilot users +160% Y/Y. $625B · +110%

- Atlassian — Q3 FY26 revenue, reported April 30, 2026. Service Collection crossed $1B ARR, +30% Y/Y. FY26 guidance raised from 22% to ~24%. $1.79B · +32%

The pattern: deterministic core compounds in low-double-digits while a high-growth AI/consumption layer scales 100%+ on top. Over half of new AI bookings come from existing customer expansion — empirical proof that AI is additive TAM, not cannibalization.

The single cleanest data point came out of Atlassian's earnings: customers who adopt the Rovo AI layer are growing their ARR at twice the rate of non-Rovo customers, and AI credit usage is growing 20%+ month-over-month. That's not cannibalization. That's the consumption layer pulling the subscription base up with it.

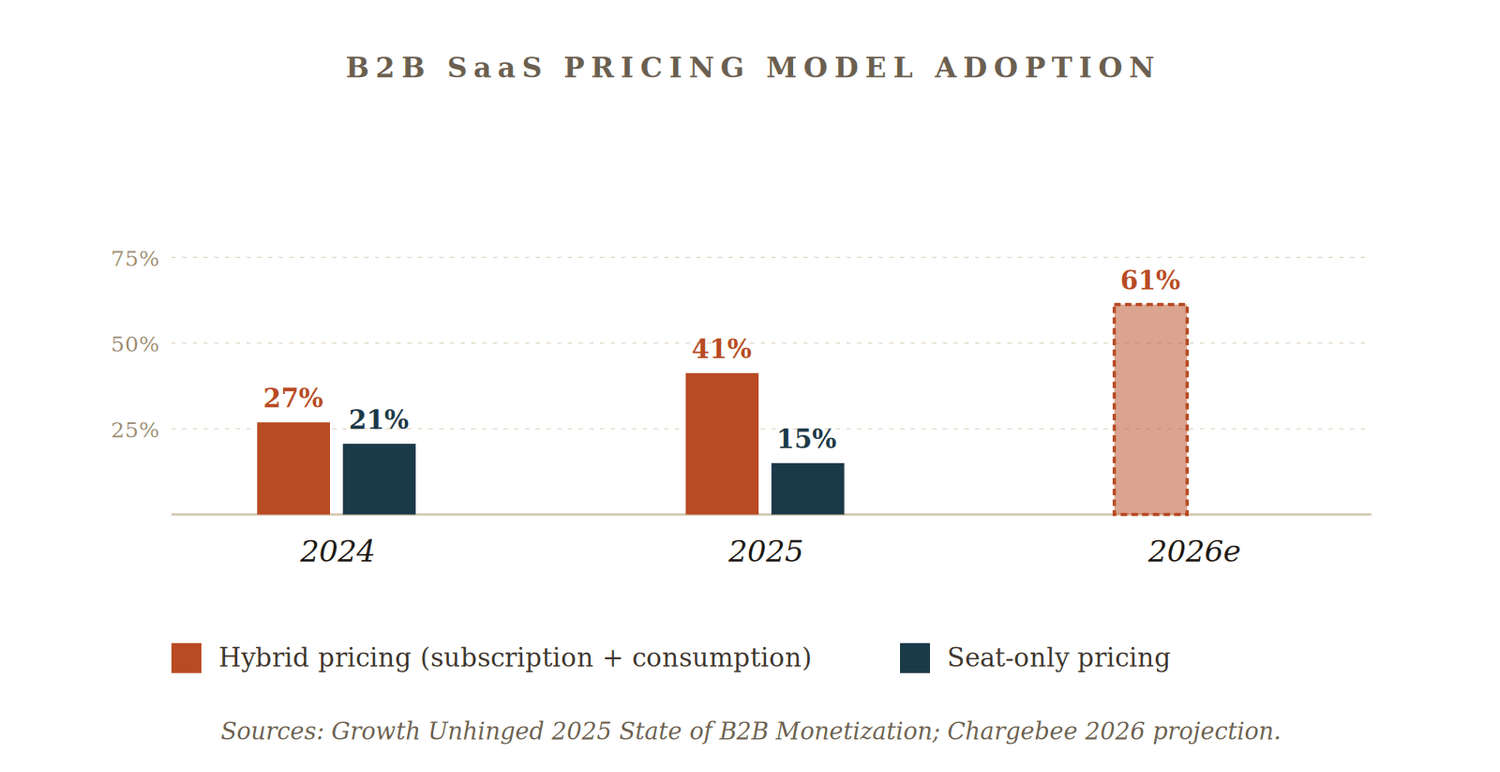

IV. Private SaaS is Following

This isn't isolated to mega-cap incumbents. It's becoming the default playbook across private SaaS.

Intercom Fin replaced per-seat with $0.99 per AI-resolved conversation. Zendesk charges per seat for humans, per resolved ticket for AI agents. Decagon, Fireflies, Synthesia, EvenUp, and Legora all price on output units — resolutions, meeting minutes, video minutes, completed legal tasks.

Companies still on pure seat-only see 2.3x higher churn and 40% lower gross margins on AI products. Bloomberg estimates subscription pricing could decline from 60% of software pricing today to 30% over the next decade — while outcome-based could climb from 10% to 60%.

That isn't a category dying. That's a category re-pricing.

V. So where does this leave us?

The bears made a clean trade on a clean story. The data is rejecting it.

Deterministic systems remain non-negotiable for the high-stakes layer of the enterprise. AI stacks on top as a force multiplier, not a substitute. Consumption pricing turns every agentic action into revenue — meaningfully larger TAM, not smaller. Public incumbents and private SaaS are running the same playbook.

The public markets are trading a narrative. The operators are building a hybrid. Bet accordingly.

Cyrus Maghami is the Founder & Managing Director of Harbor Ridge Capital, a SaaS and tech-services-focused M&A advisory firm that has completed 69 transactions representing $2.3B in value.