Across eight recent or pending SaaS take-privates (Dayforce, Olo, Smartsheet, Squarespace, SolarWinds, Couchbase, Sapiens, MeridianLink), the pattern is clear: PE is capitalizing on the current unsexy sentiment and value-pricing for vertical SaaS, despite sound fundamentals.

- KPIs: Growth ~12% YoY (median 11%), Rule of 40 ~32%, Gross Retention ~93%, NRR ~109%

- Valuation: ~6.1x revenue average (median 6.3x); EV/EBITDA where disclosed ≈ 20–25x

- Vs. Prior Peaks: Take-out prices averaged ~84% of ATH (median ~86%) — wide dispersion (Olo ~36% of ATH; Couchbase/Squarespace >100%)

- Why Go Private: nearly all of the all-time-highs were in 2021, and even with a 47% premium, they're going private only at 84% of those ATHs — four years later.

Translation: While public market investors seek AI at all costs (Palantir at ~110x revenue), savvy PE investors grounded in fundamentals see buying opportunities of mission-critical SaaS leaders at value pricing, with a clear line of sight to 2–3x in 3–5 years.

This raises the question: which undervalued yet high-quality SaaS companies are next to be taken private by Thoma or Vista? If I am to speculate, the following are in their crosshairs as we speak. This is not investment advice.

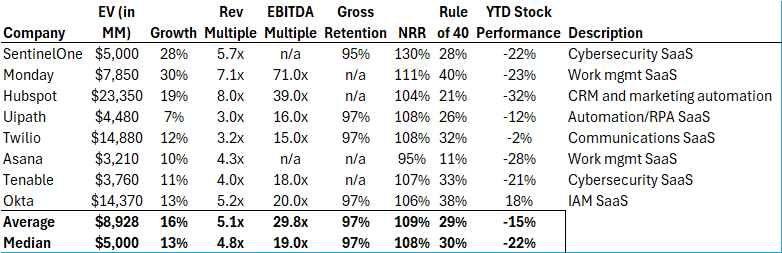

Across these potential take-privates, a few things jump out:

- Growth: stronger than those taken private, with better gross retention, the same average NRR, and nearly the same average Rule of 40 at 30%

- Valuation: at ~5x revenue these companies would line up right around 6x when factoring in the take-private premium

- YTD Stock Performance: averaging negative 15% while the Nasdaq is up 12%

- Have and Have-Nots: PE will cherry-pick the best assets at the lowest relative valuations. HubSpot has the second-lowest NRR yet the highest revenue multiple. Tenable has trending-down NRR but may be stabilizing at 107% while trading at 4x revenue with a 33% Rule of 40. Twilio has rising NRR (108%, up from 102%), which is probably why its stock is only down 2% YTD.

- Public SaaS > Overpriced Private SaaS: hundreds of private SaaS unicorns remain overvalued from peak ZIRP. For PE to make money on such a deal, they theoretically can pay no more than 5–6x revenue, and that company must have even stronger KPIs to make it an attractive IPO candidate (think Figma) for liquidity.

It will be fascinating to see how this plays out over the coming quarters — specifically whether the unsexy sentiment of SaaS persists or public-market investors gradually rotate back into the sector, encouraged by outcomes such as Wiz or Figma. Similarly, what do these take-private deals mean for the private markets, and will they reverberate downstream, level-setting valuations from the top down? Only time will tell.