AI Isn't Eating SaaS. It's Expanding It.

The bears are pricing seat compression. They're missing the consumption layer being built on top.

By Cyrus Maghami, Founder & Managing Director, Harbor Ridge Capital

The SaaS apocalypse is a tidy story. AI eats workflows. Seats compress. Systems of record become legacy. Sell the incumbents. The numbers tell a different story. So does the architecture.

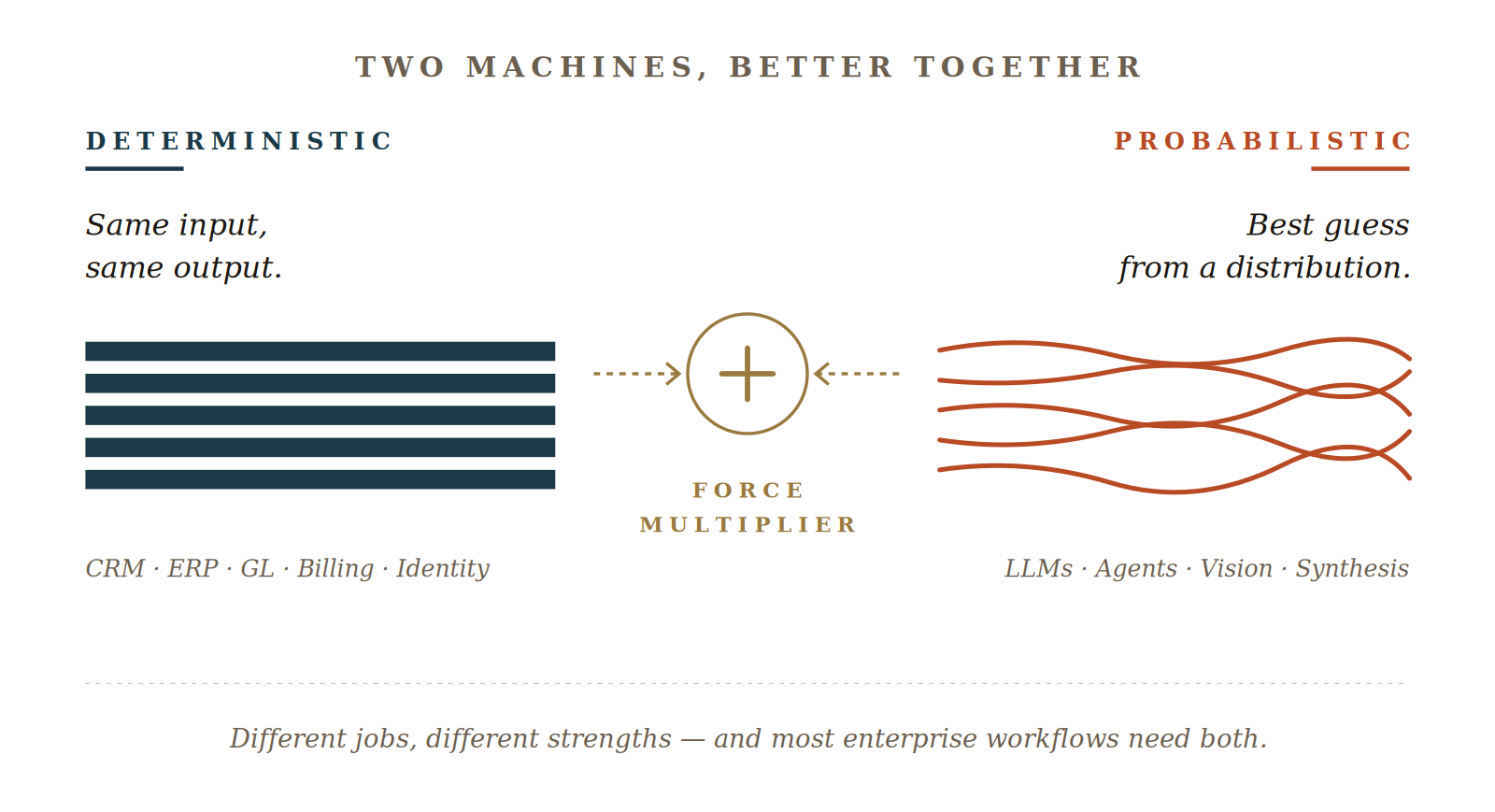

I. Two Machines, Different Jobs

Software now comes in two flavors. Deterministic systems — CRM, ERP, GL, billing, identity — do the same thing every time. Auditable, reproducible, non-negotiable in high-stakes workflows. Probabilistic systems — LLMs, agents, vision models — bring versatile judgment but are non-reproducible by design.

They aren't competitors. They complement. Where stakes are high, deterministic still wins. Where work is open-ended, probabilistic shines. In the enormous middle, they work best together — AI orchestrating across deterministic systems of record, multiplying their value rather than replacing them.

II. The Mispricing

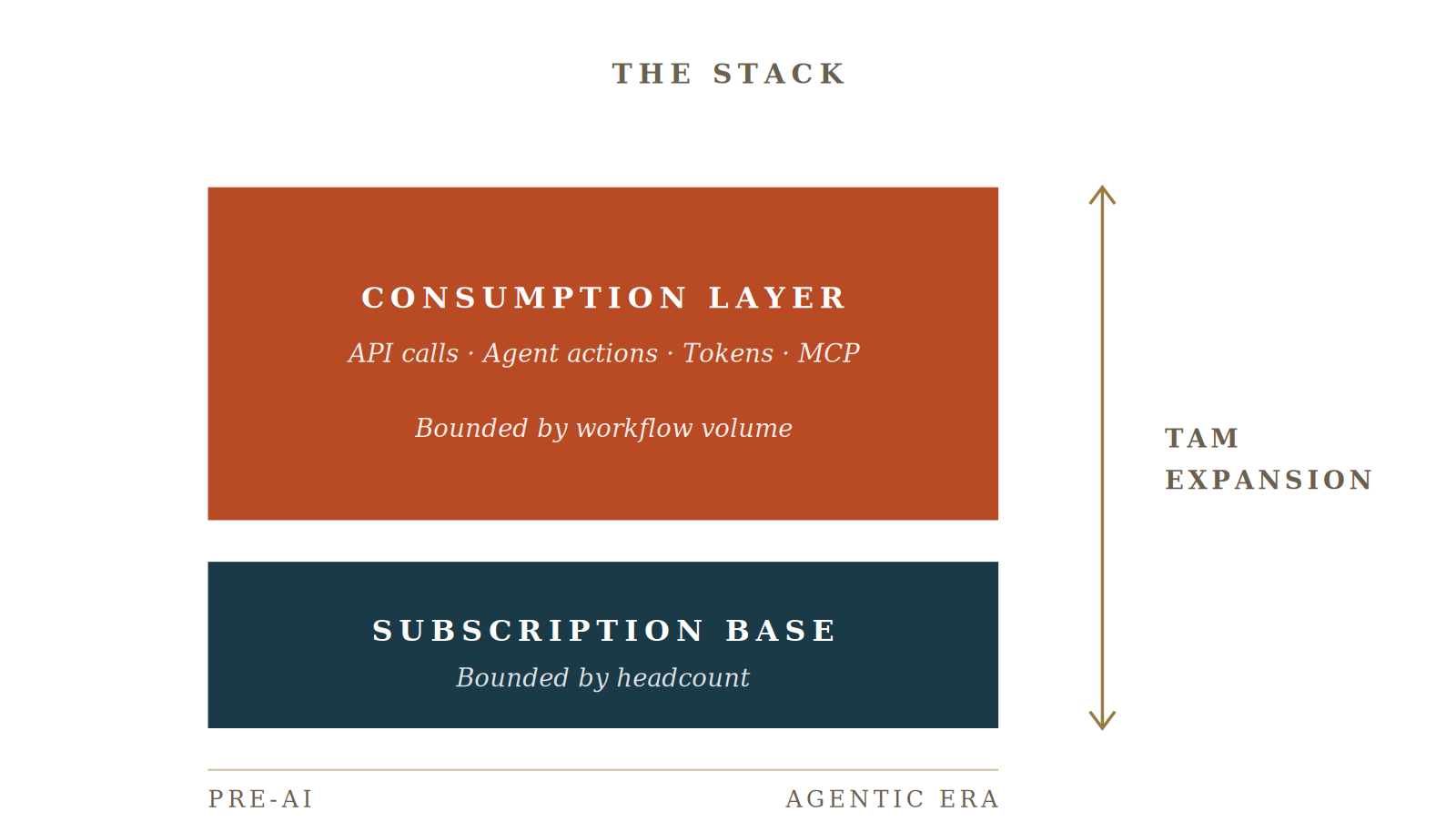

Here's what most takes miss: the agentic layer isn't just a defensive hedge for SaaS incumbents. It is structural TAM expansion.

Per-seat pricing is bounded by headcount. A 10,000-person customer has a ceiling. Consumption-based monetization — API calls, agent actions, tokens, MCP invocations — is bounded by workflow volume. Agents don't sleep, take lunch, or context-switch. They transact orders of magnitude more than humans ever did.

Every workflow that lived behind a UI as a "free" feature becomes a billable, metered unit when an agent calls it. The product surface didn't grow. The monetizable surface did.

The bear case prices the floor. It misses the new floor being built on top.

III. The Receipts

This isn't theoretical. It's already in the revenue line.

Salesforce - Agentforce ARR, Q4 FY26. Combined Agentforce + Data 360 ARR is now $2.9B, up 200%+. FY30 target raised to $63B. $800M · +169%

ServiceNow - 2026 AI ACV target, raised 50% above prior guidance. $1M+ Now Assist customers grew 130%+ Y/Y. ~$1.5B

Microsoft - Commercial RPO, Q2 FY26 — contracted future revenue. Microsoft 365 Copilot users +160% Y/Y. $625B · +110%

Atlassian - Q3 FY26 revenue, reported April 30, 2026. Service Collection crossed $1B ARR, +30% Y/Y. FY26 guidance raised from 22% to ~24%. $1.79B · +32%

The pattern: deterministic core compounds in low-double-digits while a high-growth AI/consumption layer scales 100%+ on top. Over half of new AI bookings come from existing customer expansion — empirical proof that AI is additive TAM, not cannibalization.

The single cleanest data point came out of Atlassian's earnings last week: customers who adopt the Rovo AI layer are growing their ARR at twice the rate of non-Rovo customers, and AI credit usage is growing 20%+ month-over-month. That's not cannibalization. That's the consumption layer pulling the subscription base up with it.

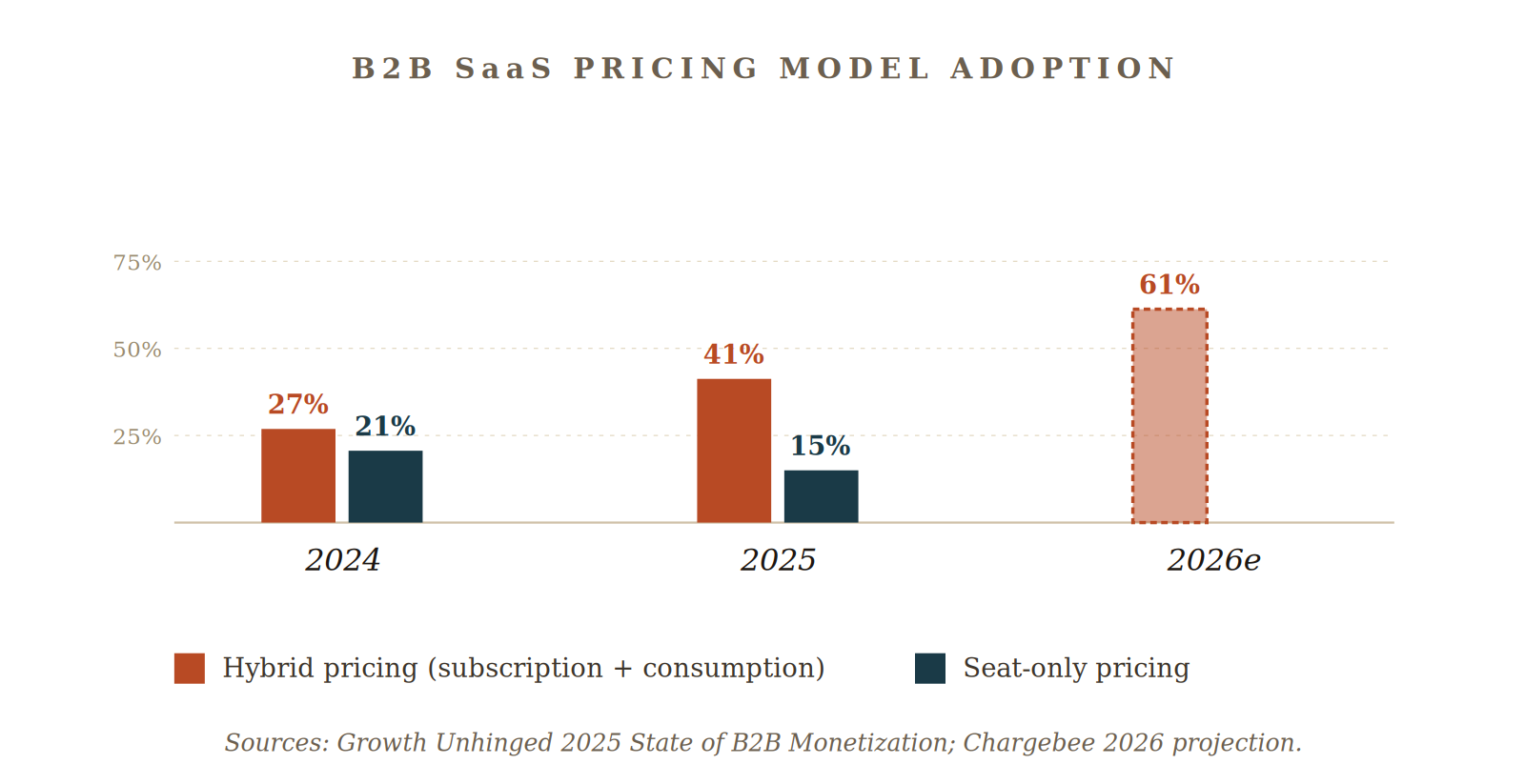

IV. Private SaaS is Following

This isn't isolated to mega-cap incumbents. It's becoming the default playbook across private SaaS too.

Intercom Fin replaced per-seat with $0.99 per AI-resolved conversation. Zendesk charges per seat for humans, per resolved ticket for AI agents. Decagon, Fireflies, Synthesia, EvenUp, and Legora all price on output units — resolutions, meeting minutes, video minutes, completed legal tasks.

The category data is striking:

Sources: Growth Unhinged 2025 State of B2B Monetization; Chargebee 2026 projection.

Companies still on pure seat-only see 2.3x higher churn and 40% lower gross margins on AI products. Bloomberg estimates subscription pricing could decline from 60% of software pricing today to 30% over the next decade — while outcome-based could climb from 10% to 60%.

That isn't a category dying. That's a category re-pricing.

V. So where does this leave us?

The bears made a clean trade on a clean story. The data is rejecting it.

Deterministic systems remain non-negotiable for the high-stakes layer of the enterprise. AI stacks on top as a force multiplier, not a substitute. Consumption pricing turns every agentic action into revenue — meaningfully larger TAM, not smaller. Public incumbents and private SaaS are running the same playbook.

The public markets are trading a narrative. The operators are building a hybrid. Bet accordingly.

Cyrus Maghami is the Founder & Managing Director of Harbor Ridge Capital, a SaaS- and tech-services-focused M&A advisory firm that has completed 69 transactions representing $2.3B in value.